Policymakers and economic development strategists are startup crazy — in pursuit of a silly goal. I know. I’ve spent most of the last decade reporting on young tech companies, exactly the slice of firm creation that has led much of the attention in this post-recession fixation.

Though I’ve taken various approaches at understanding what, if anything, is really different about this era’s of business creation, I recently found myself pulling together some data that I wanted to share.

Hype around startups — newly created businesses, particularly ones that are approaching new business models — has merit. But the concept isn’t as new and their impact isn’t yet as bold as you might hope — Millennials are on pace to be one of the least entrepreneurial generations on record.

My interest was piqued on this most recently by something Downtown Denver Partnership CEO Tami Door told me about “startups” at an event we at Technical.ly held there in February: “We had those in the 1980s, too. We just didn’t have the cute branding.”

She isn’t lying.

Reminder: today's startup enthusiasm is because we need to reverse declining economic dynamism, not because it is thriving. Start something. pic.twitter.com/rFKIYqHC39

— Christopher Wink (@christopherwink) November 12, 2016

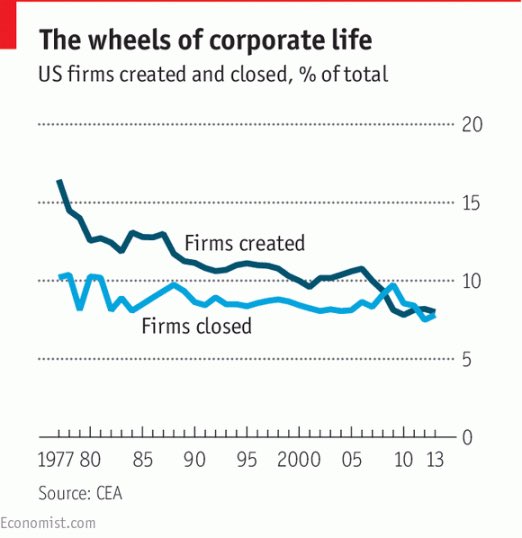

The number of new firms created between 2009 and 2011 in the United States was lower than between 1978 and 1980, according to Brookings. The rate of employing small business owners in the country has been declining since 1996, though last year saw an uptick in ones that were five years or older, which had been hurt by the recession and immigrants now make up one in five small business owners.

{kind=link}

Things have changed though since the 1980s though.

The number of small businesses in the country has grown 49 percent to 28 million since 1982, according to the federal U.S. Small Business Administration — which defines any company with fewer than 500 employees as a small one. The SBA is in the business of putting a positive spin on small business growth in the country but I do assume they approach these topics with reliability.

The first clarification you have to make with that number has become a rallying cry for the Kauffman Foundation: jobs growth in the United States isn’t so much dominated by small businesses, as is the customary line from politicians, but rather by young businesses. They can be the same but aren’t always.

Though new businesses (what we today call startups) churn employees too (meaning, they close when it isn’t working), they’re primarily responsible for net job growth and a major part of gross job growth (because more established firm success is balanced out by other older businesses closing).

This enthusiasm with startups also comes with an assumption that they’re intending to hire employees. That’s critical because the vast majority of incorporated businesses in the United States are sole proprietorships and other nonemployer firms — 22 million of those 28 million small businesses in the country.

So that’s where we see the most “small business growth” today, with the freelance graphic designer, the independent contractor oil rig worker, the Uber driver and the hair stylist, among many others. It’s the employee-free 1099 economy at work.

And it worries us. Cities that struggle with economic growth are ones that have a higher percentage of those sole proprietorships than cities that are succeeding. Contrast the rate of sole proprietorship growth from 2002 to 2012 in places like Philadelphia and Detroit (struggling, and with 64 and 59 percent growth) with Boston and New York City (succeeding, and with 24 and 34 percent) in the below chart from the Center City District in 2013.

We want new incorporations but prefer them to be of companies that intend to grow. The hope was that the Great Recession would force a new generation of entrepreneurs. Instead it may have created a missing generation of growing companies.

Still, there really was a post-recession startup (mini) boom. In March 2011, 5.5 percent, or 900,000, of self-employed people were unemployed the year before, according to the SBA. People forced out by the recession did start something new. That figure was climbing far more slowly before the recession, growing from 3.1 to 3.6 percent between 2001 and 2006. Similarly, small businesses accounted for 64 percent of net new jobs between 1993 and 2011, a share that grew modestly to 67 percent post-recession.

So though startups helped bring employment back to pre-recession levels, there is no real generational surge in new firm creation and, what’s worse, the companies that are starting continue to employ fewer people than their peers of the past. If you start a company today, you’re far more likely to make it a pass-through S Corporation or keep it a sole proprietorship than in the past, which concerns the Tax Foundation.

So the interest in startups is warranted but only insofar as it might help rebuild a culture of churn: we want regular business creation so we have the best chance of finding the most efficient uses of capital. Let the rest of them fail and have them start again. Because we know many businesses will fail, we just need those entrepreneurs to try again. Half of new businesses don’t last five years. Two-thirds don’t make it a decade and just a quarter last to the 15 year mark, according to Forbes.

We want this growth because the young ones create net jobs but the big ones create wealth and can have staying power. Look at the below chart I created using this SBA data. Companies that grow to 20 employees or more start representing proportionally more of the country’s payroll than their smaller peers.

Much of this doesn’t fit neatly into the national conversations around entrepreneurship, one that suggests the tech founder of today is a one of a kind and its rapid scale holds the future.

It’s true that a national fixation on startups helpfully boosts company founding as a priority for economic development, but it lacks the nuance of the goal. We also are ignoring the hard reality that the energy around startups in recent years has only been a desperate thrashing in response to the sinking ship that was our recession-induced global economy.

If you’re picturing an entrepreneur you know (or even picturing yourself), her work is absolutely vital to economic growth, no doubt. But rather than something new, it is something old that we need far more of. (Don’t shoot to start a one-person firm, which is far more common. Aim to build a company that employs people).

Indeed, the innovation clustering many people in my circles talk about is happening, nearly exclusively in large urban centers. But concerningly, even those successes are still just a holding pattern, not progress. Strong unemployment numbers are being hidden by the lowest labor participation rate in a generation — dating from a time when many women were still not active in the workforce. Look at a more recent look above in the graph from the Bureau of Labor Statistics. We’re still sinking.

This “employment bomb” is still a concerning weight on our economic future. No doubt our startup fixation can be focused with purpose. We do need far more dynamism in our economy. Whether that will be enough to face up against looming macroeconomic and societal shifts is something we’ll likely only know a generation or two from now.